Three numbers define every insurance policy you’ll ever buy — the premium, the deductible, and the coverage limit. Most people who have been buying insurance for years couldn’t give a precise definition of all three, which is less a reflection of their intelligence than of how rarely insurance is explained clearly rather than sold aggressively. Understanding exactly what each number means, how the three interact with each other, and how changing one affects the others is the foundation of every intelligent insurance decision — from choosing a policy to filing a claim to evaluating whether your current coverage still makes sense.

This guide explains all three with the specificity that makes them genuinely useful rather than just technically understood.

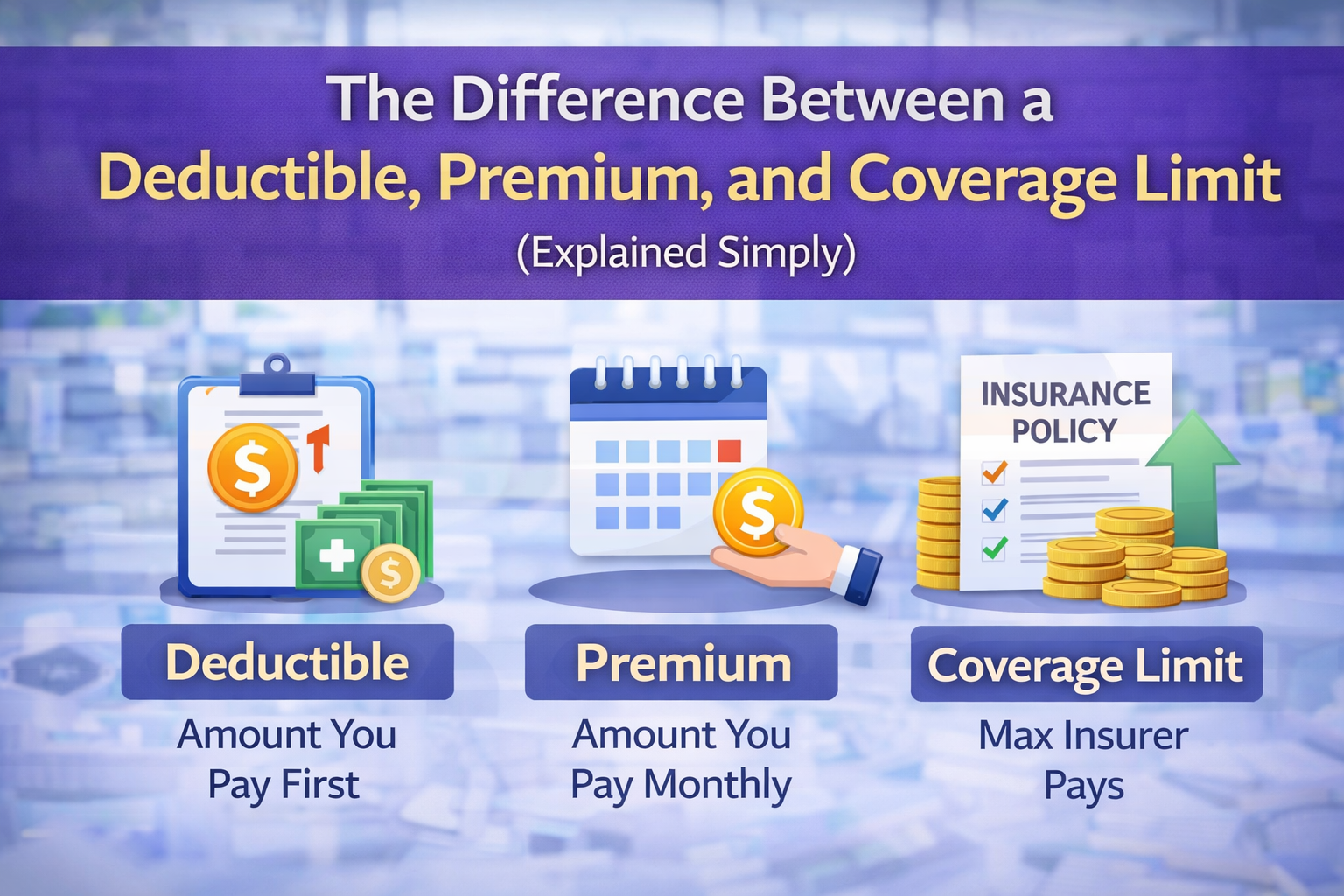

The Premium: What You Pay to Have the Coverage

The premium is the amount you pay the insurance company for the coverage the policy provides — monthly, quarterly, or annually depending on how the policy is structured. It’s the only number in the three that you pay regardless of whether anything bad happens, which is why it’s the number most people focus on when comparing policies and the number that insurance companies compete most visibly on in their advertising.

What the premium actually represents is the insurance company’s assessment of how much it will cost, on average, to cover you — factoring in the probability that you’ll file a claim, the expected cost of that claim if you do, and the company’s operating costs and profit margin. When an insurance company quotes you a higher premium than another company for identical coverage, it’s because their risk assessment of your specific profile produces a different expected claim cost. When your premium increases at renewal without any apparent change in your circumstances, it’s almost always because either your risk profile changed in ways you may not have noticed or the company’s overall loss experience in your area or category changed.

The premium is the most visible insurance cost but rarely the most important one for evaluating the actual value of a policy. Two policies with different premiums can represent dramatically different value depending on what the coverage limit and deductible look like — which is why premium comparisons without looking at the full policy structure produce the kind of false economy that leaves people underinsured at a lower monthly cost.

The Deductible: What You Pay When Something Goes Wrong

The deductible is the amount you pay out of pocket before the insurance company begins paying a covered claim. If your car insurance has a $1,000 collision deductible and you have an accident that causes $4,000 in damage, you pay $1,000 and the insurance company pays $3,000. If the damage is $800 — less than your deductible — the insurance company pays nothing and you cover the full $800 yourself.

The deductible’s primary function in insurance design is risk sharing — it ensures that the policyholder absorbs a portion of every claim rather than having the insurance company cover every loss from the first dollar. This serves two purposes simultaneously. It reduces the premium because the insurance company’s expected payout is lower when the policyholder is absorbing the first portion of every claim. And it reduces the frequency of small claims that would cost more to administer than they’re worth — nobody files a claim for a $200 scratch when they have a $500 deductible.

The deductible decision is fundamentally a financial trade-off between certain savings now — a lower premium from a higher deductible — and uncertain costs later — the higher out-of-pocket expense if a claim occurs. The math that makes this trade-off rational is straightforward. If choosing a $2,000 deductible over a $500 deductible saves $400 per year in premium, and if you file one claim every five years on average, you save $2,000 in premiums over that period while potentially paying $1,500 more in deductible costs — a net saving of $500. If you file claims more frequently, the higher deductible costs more than it saves.

The deductible decision becomes less about math and more about financial resilience when the higher deductible requires paying out of pocket at a moment when the financial pressure is already significant. A $2,000 deductible is a rational financial choice for someone with $10,000 in emergency savings and a much less rational one for someone with $500. The premium savings from a higher deductible should always be evaluated against the realistic ability to pay that deductible at the worst possible moment — which is, by definition, when a claim occurs.

One important distinction that catches policyholders off guard is the difference between per-occurrence deductibles and annual deductibles. Auto and homeowners insurance typically use per-occurrence deductibles — you pay the deductible each time a separate claim is filed. Health insurance typically uses an annual deductible — you pay out of pocket until you’ve reached the deductible amount for the year, and then the insurance covers costs above that threshold for the remainder of the year. The practical difference is significant — a health insurance annual deductible of $3,000 means the first $3,000 in medical costs each year comes entirely from your pocket, regardless of how many separate medical events produce those costs.

The Coverage Limit: The Maximum the Insurance Company Will Pay

The coverage limit is the maximum dollar amount the insurance company will pay for a covered loss — and it’s the number that matters most when a major claim actually occurs, which makes it the most underexamined of the three in most insurance purchase decisions.

Coverage limits exist at multiple levels depending on the type of insurance. A homeowners policy might have a $400,000 dwelling coverage limit — the maximum it will pay to rebuild the home — alongside a $100,000 personal liability limit and a $50,000 personal property limit. An auto policy might have a $100,000 per-person bodily injury limit, a $300,000 per-accident bodily injury limit, and a $100,000 property damage limit. Each limit applies independently to the category it covers, which means a claim can exceed the limit in one category while remaining well below the limit in another.

The coverage limit problem that most policyholders experience is discovering after a claim that the limit that seemed adequate at policy purchase is inadequate given the actual cost of the loss. This happens in two common scenarios. The first is the underinsured home — a homeowner who insures the house for its market value rather than its replacement cost discovers after a total loss that rebuilding costs significantly more than the policy pays out, because construction costs have increased and market value doesn’t equal replacement cost. The second is the inadequate liability limit — a policyholder with a $100,000 liability limit who causes an accident resulting in $300,000 in injuries is personally responsible for the $200,000 difference between the claim and the limit.

Setting coverage limits requires modeling the worst realistic outcome rather than the average one. The question that produces the right liability limit is not “what does the average car accident cost?” but “what would a serious accident with significant injuries cost, and could I personally absorb anything above my coverage limit?” For most people, the honest answer to the second question is no — which means adequate liability limits are one of the most important and most frequently underestimated aspects of insurance coverage.

How the Three Numbers Interact With Each Other

The premium, deductible, and coverage limit don’t exist independently — they’re connected through a set of relationships that understanding makes every insurance decision more productive.

The most direct relationship is between the deductible and the premium. Higher deductibles produce lower premiums because the insurance company’s expected payout is lower when the policyholder absorbs more of each claim. Lower deductibles produce higher premiums because the company pays more of every claim. This relationship is predictable and calculable, which is why comparing policies with different deductibles requires adjusting for the premium difference rather than comparing deductibles in isolation.

The relationship between coverage limits and premiums is similar but less symmetrical. Increasing a liability limit from $100,000 to $300,000 typically adds much less to the premium than the coverage increase might suggest — because the probability of a claim reaching $300,000 is lower than the probability of a claim reaching $100,000, and the premium reflects that probability difference. This asymmetry means that increasing coverage limits is often more cost-effective than people assume, and underinsuring to save on premiums at the coverage limit level is a worse trade-off than underinsuring at the deductible level.

The relationship between all three and the actual value of the policy is where most insurance purchase decisions fall apart. A policy with a low premium, a high deductible, and a low coverage limit might appear affordable until a major claim reveals that the low premium was purchased with the certainty of high out-of-pocket costs and inadequate recovery. Evaluating the three together — the total cost of the premium plus the expected deductible cost plus the exposure above the coverage limit — produces a more accurate picture of what a policy actually costs and provides than any single number comparison does.

The Practical Application: Using These Three Numbers to Compare Policies

Understanding the three numbers in isolation is useful. Using them together to compare policies is where the understanding produces financial value.

When comparing two auto insurance quotes, the comparison that matters is not which policy has the lower premium. It’s which policy produces the better outcome across the range of scenarios you’re realistically likely to face. A policy with a $500 lower annual premium and a $1,000 higher deductible is a better value if you have a strong emergency fund and file claims infrequently. It’s a worse value if your financial cushion is thin and a $1,500 deductible at claim time would create genuine hardship.

When evaluating coverage limits, the comparison that matters is not which policy has limits that seem adequate in the abstract. It’s which policy provides limits adequate to cover the realistic worst-case outcome — and whether the premium difference between adequate and inadequate limits is worth paying. In most cases, the answer is yes, because the premium difference for higher limits is modest and the financial exposure of inadequate limits is potentially catastrophic.

The single most productive insurance exercise most people can do is reviewing their current policies with these three numbers as the framework — not to find the cheapest coverage but to confirm that the deductible is a number they could realistically pay at a bad moment, the coverage limit is a number that would actually cover a major loss, and the premium represents the cost of genuine protection rather than the cost of technically having a policy.

What Knowing This Changes

Understanding the premium, deductible, and coverage limit doesn’t make insurance shopping effortless. Insurance policies are still complex documents with exclusions, conditions, and endorsements that affect coverage in ways that the three main numbers don’t capture. But understanding the three numbers changes the starting point for every insurance evaluation from confusion to a clear framework — and that framework makes every subsequent insurance decision more grounded in what the policy actually does rather than what the premium suggests.

The most expensive insurance mistakes — the ones that leave people facing five- and six-figure out-of-pocket costs after a major loss — almost always trace back to a misunderstanding of one of these three numbers. A deductible that wasn’t affordable at claim time. A coverage limit that was set at a number that felt large without being adequate. A premium that was optimized at the expense of the protection it represented. Knowing the difference prevents those mistakes before they happen rather than explaining them after.

Now that the three core numbers make sense, the next question most people have is why their specific premium is higher than they expected — and what they can legally do about it. Our guide on how insurance companies decide what you pay — and how to use that knowledge to lower your rate covers the specific factors that drive premium calculations and the legitimate strategies that produce real savings without reducing real coverage.

Which of these three numbers — premium, deductible, or coverage limit — has caused the most confusion or the most unexpected cost in your insurance experience? Leave a comment with the specific situation. Real examples from real policyholders help us make these explanations more useful for everyone who reads them.

Leave a Reply