The most common reason young and healthy people give for not buying life insurance is that they don’t need it yet — and for a specific subset of young people, that reasoning is correct. A twenty-five-year-old with no dependents, no significant debt, and no one whose financial security depends on their continued income genuinely doesn’t need life insurance in the way that a thirty-five-year-old with a mortgage, a spouse, and two children does. The insurance exists to protect financial dependents from the loss of the income they depend on — and without dependents, the protection argument is genuinely weaker.

But the argument against buying life insurance young is not the same as the argument for waiting until the need is undeniable — and the difference between those two positions is the thousands of dollars that most people who wait unnecessarily pay in higher premiums over the full life of their coverage compared to what they would have paid if they had purchased earlier. Understanding the specific financial mechanics of the age-premium relationship, the health-premium relationship, and the insurability risk that increases with time produces a more complete picture of the young and healthy buyer’s actual situation than the simple “I don’t need it yet” conclusion.

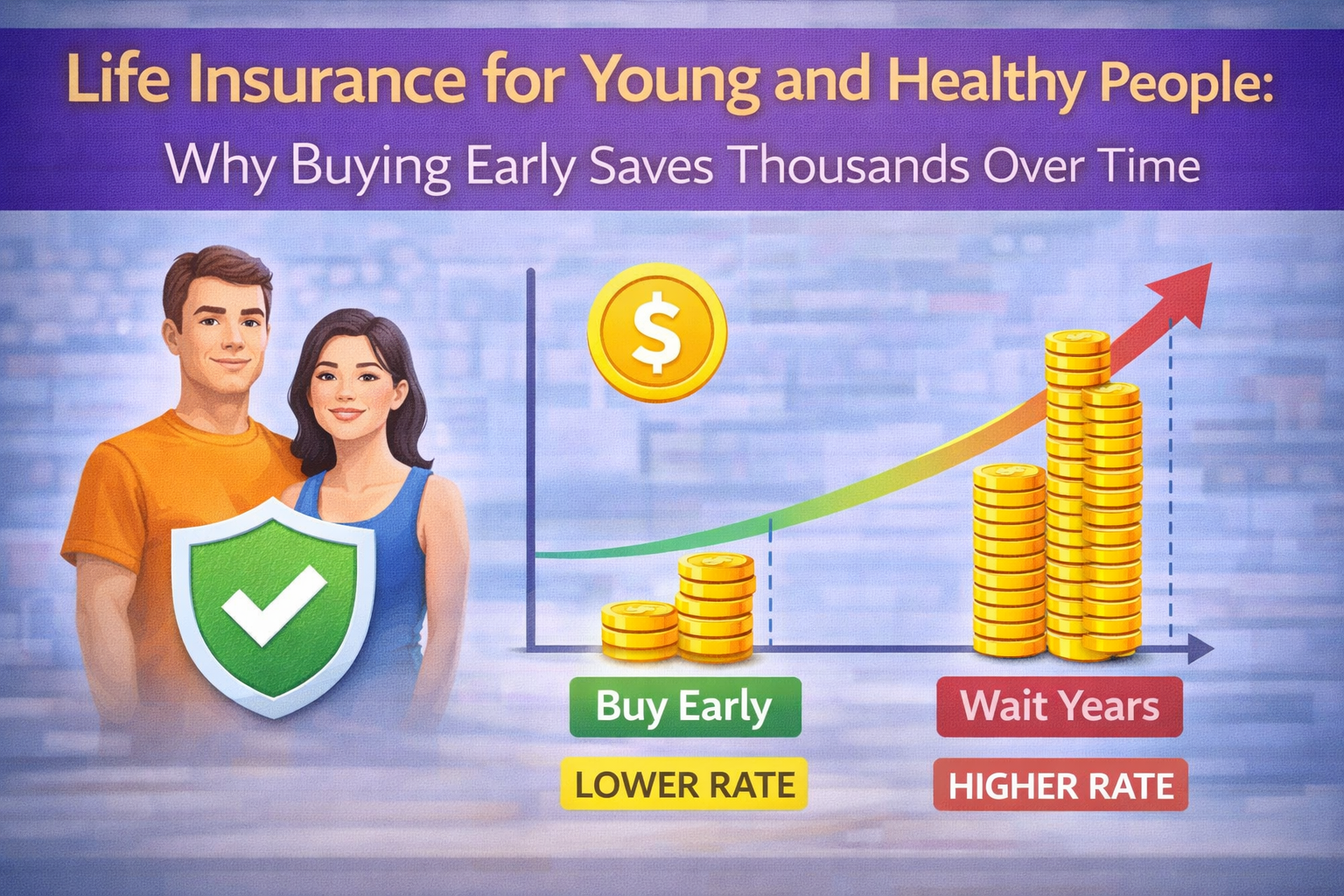

The Age-Premium Relationship That Makes Early Purchase Financially Compelling

Life insurance premiums are priced primarily on mortality risk — the statistical probability of the insured dying during the coverage period — which increases with age in a predictable pattern that actuarial tables have documented across decades of claims experience. The premium for a given coverage amount increases with every year of age at application, producing a cumulative cost difference between purchasing at twenty-five and purchasing at thirty-five that is substantial enough to justify early purchase even when the financial need is less urgent.

The specific numbers illustrate the relationship more clearly than the general principle. A healthy twenty-five-year-old non-smoking male applying for a $500,000 thirty-year term policy might pay approximately $20 to $22 per month — $240 to $264 per year. The same healthy non-smoking male at thirty-five applying for the same $500,000 thirty-year term policy might pay approximately $32 to $38 per month — $384 to $456 per year. The premium difference of $12 to $16 per month compounded over the thirty-year term represents a total premium difference of $4,320 to $5,760 for identical coverage — a difference that exists entirely because of the ten-year delay in purchase.

The premium difference widens as the age at application increases — the gap between purchasing at twenty-five and purchasing at forty-five is significantly larger than the gap between twenty-five and thirty-five, because the mortality risk acceleration that actuarial tables document is not linear. The premium for a forty-five-year-old male purchasing the same $500,000 coverage might be $80 to $100 per month — three to four times the premium for the same coverage purchased at twenty-five. The cumulative premium difference over a comparable coverage period represents tens of thousands of dollars in additional premium cost for identical protection.

The Health Premium Relationship That Makes Young Purchase Even More Valuable

Age is the most predictable factor in life insurance pricing — but health status is the factor that creates the most dramatic premium differences between individuals at the same age, and the relationship between age and health creates a specific dynamic that makes early purchase more valuable than the age premium difference alone suggests.

Health status at the time of application determines which underwriting classification the applicant receives — preferred plus, preferred, standard plus, standard, or substandard — and the premium difference between classifications is significant enough to be a meaningful financial consideration. The healthiest applicants at preferred plus classification pay approximately 40% to 60% less than standard classification applicants of the same age — a difference that reflects the mortality risk differential between excellent and average health profiles.

The dynamic that makes young purchase particularly valuable is the correlation between age and health status — young people in their twenties and early thirties are more likely to qualify for preferred and preferred plus classifications than the same individuals will be at forty or forty-five, because the health events that degrade insurance classification — high blood pressure, elevated cholesterol, diabetes, obesity, sleep apnea — are less prevalent in younger age groups and more common in middle-aged ones. The twenty-five-year-old who is currently in excellent health and would qualify for preferred plus classification may be in a different health category at thirty-five — not because of any catastrophic health event, but because of the gradual health changes that accumulate during a decade of adult life.

Purchasing life insurance when the health profile supports the best available classification locks in that classification for the life of the policy — the premium paid at preferred plus at twenty-five doesn’t change to reflect deteriorating health at thirty-five, because the premium is fixed at application rather than annually adjusted. The young buyer who is currently in the health category that produces the best pricing locks that pricing in for the full term regardless of what happens to health between purchase and the end of the term.

The Insurability Risk That Most Young People Don’t Consider

The most underappreciated argument for buying life insurance young and healthy is not the premium savings — it’s the insurability risk that increases with time. Insurability is the ability to obtain life insurance at standard rates or better — and it’s not guaranteed for everyone at every age. The health events that affect insurability are not always predictable, not always preventable, and not always minor enough to leave insurability intact.

A cancer diagnosis, a heart attack, a stroke, a serious autoimmune condition, or a significant mental health diagnosis can make life insurance either uninsurable or insurable only at substandard rates with significant premium surcharges. These events are uncommon at any given age but become increasingly probable across a decade of life — the probability that a currently healthy twenty-five-year-old will experience a significant health event between twenty-five and thirty-five is not negligible when considered across the full range of possible events that affect insurability.

The young person who defers life insurance purchase until the financial need is unambiguous — until there are dependents, until there is a mortgage, until the financial picture requires protection — takes the risk that the health status that currently makes them an attractive insurance applicant will still be intact when the purchase becomes urgent. The person who purchases at twenty-five, when the health profile is excellent and the premiums reflect that health, eliminates the insurability risk for the coverage purchased regardless of what health changes occur between twenty-five and the end of the policy term.

The Financial Dependent Scenario That Changes the Calculus Immediately

The abstract premium savings argument for early life insurance purchase becomes concrete and urgent the moment financial dependents enter the picture — and the speed with which that transition occurs is faster than most young people anticipate when they defer the purchase until the need feels immediate.

A young couple who purchases a home with a mortgage creates a financial dependency — the surviving partner’s ability to maintain the mortgage payment and the housing stability it provides depends on the continued income of both partners. The marriage itself creates an interdependency — the financial plans that the couple has built together, including the retirement savings strategy, the housing decisions, and the lifestyle expectations, are built around two incomes and are disrupted by the loss of one.

A pregnancy creates an immediate financial dependency that begins before the child arrives — the financial planning for the child’s arrival includes the income replacement that life insurance provides for the parent who doesn’t survive to raise the child they planned for. The couple who defers life insurance purchase until the child is born has created a dependency and taken the application risk without the coverage in place during the pregnancy — a period that typically represents months of uninsured dependency.

The recommendation that emerges from this dynamic is to purchase life insurance at the earlier of two trigger points — the age at which the financial profile makes early purchase financially compelling given the premium savings potential, or the point at which financial dependencies make the coverage urgent. For most people, the first trigger point arrives in the mid-to-late twenties when excellent health makes coverage most affordable. The second trigger point should never arrive without the coverage already in place.

How Much Coverage Young Buyers Actually Need

The coverage amount calculation for young buyers follows the same framework described in the previous guide — but with specific considerations that apply to earlier life stage purchases that affect the inputs into the DIME or income replacement calculation.

Young buyers with minimal existing financial obligations — no mortgage, no dependents, limited debt — may genuinely need less coverage than the DIME calculation produces for more financially encumbered buyers. A twenty-five-year-old purchasing life insurance primarily to lock in pricing while in excellent health might purchase a smaller initial policy — $250,000 to $500,000 — with a conversion option that allows increasing coverage without new medical underwriting as the financial obligations and dependencies grow.

The conversion option is the feature that makes an early smaller purchase more strategically valuable than it would otherwise be — because the ability to convert term coverage to permanent coverage or to increase coverage without new underwriting allows the initial purchase to serve both the current modest need and the future larger need without requiring the buyer to re-enter the underwriting process when health may have changed.

Young buyers who already have significant financial obligations — a mortgage, a spouse, young children — should apply the full DIME or needs analysis calculation rather than purchasing a smaller initial policy, because the financial dependency that exists today requires the coverage that addresses it today rather than a placeholder policy that will need to be supplemented later.

The Employer Group Life Insurance Misconception

Many young workers rely on employer-provided group life insurance as their primary or only life insurance — a reliance that creates a specific vulnerability that most don’t recognize until the vulnerability matters.

Employer group life insurance is a valuable benefit — typically one to two times annual salary — but it has two structural limitations that make it inadequate as a standalone life insurance solution. The first is the coverage amount — one to two times annual salary is typically well below the coverage target produced by any serious needs analysis, and the gap between the employer benefit and the actual coverage need is the individual life insurance gap that employer benefits don’t address.

The second limitation is portability — employer group life insurance coverage exists as long as the employment relationship does, and ends when the employment relationship ends. A young worker who relies entirely on employer group coverage and loses the job — whether through voluntary resignation, layoff, or disability — loses the life insurance coverage simultaneously. The COBRA continuation that extends health insurance doesn’t extend life insurance, and converting group coverage to individual coverage at separation is typically available but at rates that reflect the loss of the group pricing advantage.

The young worker who supplements employer group coverage with an individual term policy addresses both limitations — the individual coverage fills the gap between the employer benefit and the actual coverage need, and the individual policy remains in force regardless of employment changes. The coordination of employer and individual coverage produces a total coverage level that matches the actual need without depending on the continuation of any specific employment relationship.

The Conversation Most Young People Avoid and Why It’s Worth Having

Life insurance purchase requires engaging with the concept of one’s own premature death — and that engagement is uncomfortable enough that many young people defer the conversation indefinitely rather than completing a purchase that would take less than an hour and that would protect the people who would be most affected by the event being contemplated.

The discomfort is understandable and doesn’t make the deferral financially rational. The family that loses a young parent to an unexpected death in year one of the deferred period faces the financial consequence of the deferral regardless of the emotional reason for it. The premium savings that the early purchase would have produced are irretrievably lost. The insurability that existed at the time of deferral may or may not still exist at the later purchase date.

The hour spent completing a life insurance application at twenty-five or thirty — when the health profile makes the pricing most favorable and the coverage most accessible — is an hour that produces financial protection for the people whose financial security depends on the applicant’s continued income. That protection is worth the discomfort of the conversation it requires to obtain.

The timing of the life insurance purchase is one dimension of the coverage decision — what happens to the coverage if premiums stop being paid is another dimension that most buyers don’t think about at purchase but that affects the coverage’s reliability over the full term. Our guide on what happens to your life insurance if you stop paying premiums covers the specific policy provisions that determine what coverage remains when payments are interrupted, so the protection that was purchased doesn’t disappear unexpectedly when financial circumstances change.

Bought life insurance young and locked in a rate you’re now grateful for — or deferred the purchase and then faced health changes that affected your insurability or your premium classification? Leave a comment with what happened. Real experiences with the timing of life insurance purchases are the most useful information available for young people who are making the same decision now.

Leave a Reply